Accounting for Branch Operations

A- Procedure

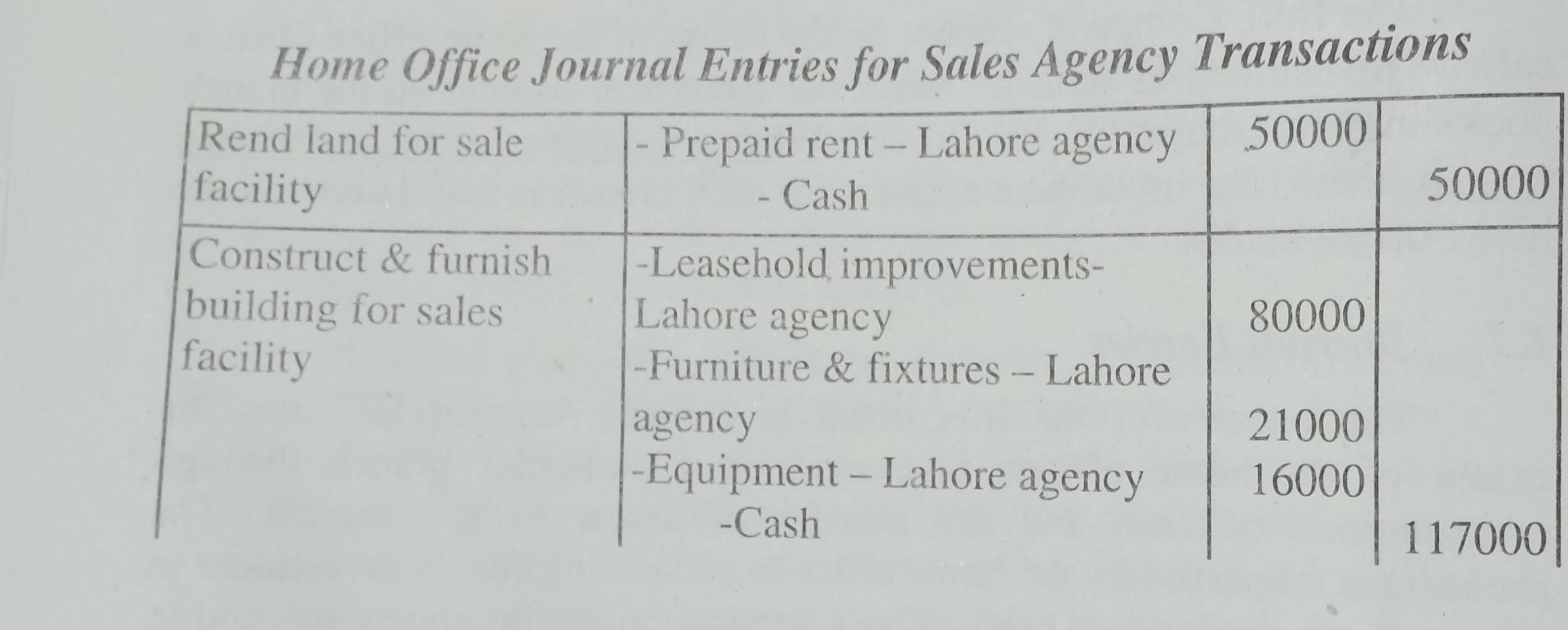

Occasionally, accounting for branch operations is centralized

at the home office, and the procedures followed are similar to those for a

sales agency. If such an approach is used the branch maintains only limited

accounting records and submits source documents for transactions to the home

office for entry in the centralized accounting system, just like sale agencies.

Balance Sheet Accounts:

a) Assets

b)Liabilities

c)Owner's Equity

B- Maximum Branches

Normally and especially with larger branches, the home office

and branches maintain separate accounting systems. Each maintains a full set of

books with a complete self-balancing set of accounts. Each records its

transactions with external parties in its own accounting system. These

transactions are recorded in the normal manner, and no special treatment is

needed. In addition, the home office and branch both must record transactions

with one another in their respective accounting systems.

Even though the home office and each branch maintain separate

books, all accounts are combined for external reporting in such a way that the

external financial statements represent the company as a single economic

enterprise. As with the preparation of consolidated financial statements,

simply adding together the balances of the accounts contained in each The accounting system does not result in the portrayal of a single economic entity.

Certain eliminations are needed as the home office and one or more branches is

quite similar to the preparation of consolidated financial statements.

Intra Company Accounts

Transactions with external parties are recorded in the normal

manner. Transactions between the home office and a branch also are treated in

a normal manner except they are maintaining its record in intracompany

accounts. These accounts are reciprocal accounts between the home office and

the branch. When the books of both the home office and the branch are

completely up to date, the balance in an intracompany account on the home

office books will be equal but opposite that of their related intracompany

account on the branch books. For example, if an intracompany account on the

home office books has an Rs. 10000 debits balance the related Intra Company

account on the branch books should have a credit balance of the same amount.

The Intra Company account on the books of the home office

often is called "Investment in Branch", while the reciprocal account

on the branch books may be labeled "Home Office". When a company has

more than one branch, a separate investment account for each branch is

maintained on their home office books.

Income Statement Accounts:

a) Operating Revenue

b) Operating Expenses

c) Non-Operating Revenues and Expenses

d) Non-Operating Expenses and Losses

Journal Entries

The balance of the Investment in Branch Account indicates the extent of the home office's investment in a particular branch through

contributions of cash and the transfer of assets to the branch. The procedures

employed by the home office in accounting for its investment in a branch are

similar to a head office's application of the equity method in accounting

for its investment in a subsidiary. The reciprocal home office account on the

books of the branch represent the home offices equity in the branch and the

balance is shown in place of owners’ equity in the separate financial

statements of the branch prepared for internal reporting purposes.

The balances of the

two reciprocal accounts are adjusted for the same transactions. The account

balances are increased for asset transfers from the home office to the branch

and reduced for asset transfer from the branch to the home office. Adjustments

to the accounts also are made for profits and losses of the branch, with branch

profits leading to an increase in the accounts balances and branch losses

leading to a decrease. Note that increases in the home office's investment in

branch account are accomplished with debit entries and decreases with credit

entries. The opposite is true with respect to the branch's Home Office account.

The reciprocal nature of the Investment in Branch and the

Home office accounts, and the way in which they are affected by various

transactions can be shown as follows:

Entries on Establishment of Branch

When a company establishes a branch, the home office in the investment in branch account records the transfer of assets to the branch. i Similarly, the branch records the transfer with an entry in the account called home office account. To illustrate, assume that the Shah corporation of Islamabad establishes a branch in Mardan. The home office transfers to the branch Rs.20000/- in cash, new office equipment that cost Rs.5000/-. and new store equipment at a cost of Rs. 30000. The Home office records the transfer with the following entry:

Home Office Entries for Branch Accounting:

Double Entry System in Branch Accounts:

1 comment:

Excellent way guide to full understanding and method of solving problems in ease.

Always available for help when mailed

Post a Comment